While financial advisors and other people in the investment industry often refer to compulsory savings and discretionary savings, many people are often not sure what the difference is between the two.

To put it briefly:

- Compulsory savings refers to retirement savings and

- Discretionary savings refers to non-retirement or optional savings.

In this article we will review the characteristics is each type of savings and the relevant implications.

Compulsory savings

Depending on an individual’s circumstances compulsory/retirement savings are typically made to a pension or provident fund, if you are an employee, and to a retirement fund if you are self-employed or if your employer does not have any retirement arrangements in place. Employees can also supplement their retirement savings be contributing to a retirement annuity.

Tax Savings

As individuals who save for their retirement are lessening the burden on the state, the Government offers certain tax incentives on these savings. This is very necessary as it is currently estimated that only about 6% of South Africans will be able to retire financially – meaning that 94% of people will have to either:

- rely on a state pension of R1 890/month.

- rely on their families for financial support.

- continue working well after the age that they intended to retire.

The incentive that the government offers is in the form of

- a tax deduction of the amount the compulsory savings up to a maximum of (the lesser of 27.5%) of your annual taxable earnings or R350 000 per year.

- The growth of the funds within the retirement vehicles are tax free. There is no tax on interest or dividends or capital gains tax (CGT) which is usually applicable to discretionary savings.

Compulsory savings have certain restrictions regarding the withdrawal and transfer of these funds as well as how they may be invested.

Access restrictions

There are restrictions accessing retirement funds both before and at retirement.

Before retirement

Before retirement age a member is allowed one full or partial withdrawal from their retirement fund. The earliest retirement date is usually 55, although this is subject to the fund rules. If a member withdraws an amount before their retirement age the amount is subject to tax according to a table defined by SARS.

At retirement

At retirement, a member is limited to accessing one third of the accumulated funds and is required to buy an annuity with the remaining two thirds. This may be a living or a life annuity. To understand more about the difference of these annuities please refer to our article Retirement Annuities Explained.

Any lump sum withdrawn at retirement is taxed by SARS according to another table defined by SARS, however, this table is more generous than the taxation on amounts withdrawn before retirement age.

Investment Restrictions

As mentioned above, one of the restrictions on these funds is that when the funds are invested, they have to comply with Regulation 28 (a requirement of the Pension Fund Act). Regulation 28 limits the extent to which retirement funds may invest in particular assets or in particular asset classes. The main purpose is to protect the members’ retirement provision from the effects of poorly diversified investment portfolios.

While there are talks about amending Regulation 28, as it currently stands, the regulation limits equity exposure in retirement funds to 75% whether local or offshore. Further, exposure to local or international property is limited to 25%, while foreign investment exposure is limited to 30%. There are also additional sub-limits for alternative investments and the percentage of a portfolio that can be held in offshore, among others.

Despite these restrictions, recent research by one of the major financial institutions comparing the returns generated compulsory funds to discretionary funds revealed that the returns are generally higher in compulsory fund – because of the tax advantages.

Protection from Creditors

During the lifetime of the member and whilst the funds are invested in the retirement fund, they are protected against the creditors of the members.

Once the member retires from the fund, any lump sum and income received from an annuity can be attached by the member’s creditors.

Upon death of the member prior to retirement, the retirement fund proceeds will be protected as long as there is a dependent to receive the proceeds (dependants include the spouse, children and those that can prove financial dependency).

If the proceeds are payable to a nominated beneficiary (other than the dependant defined above), the trustees of the retirement fund will be obliged to first settle any debts (insofar the aggregate liabilities exceed the aggregate assets in the estate) before making payment to that nominee.

Discretionary Savings

As the name suggests discretionary savings is often used to describe money that is not designated for a particular purpose. It is up to the owner of the discretionary funds to decide how they should be invested and spent.

The options in which to invest discretionary funds are almost unlimited and include savings accounts, bonds, shares, EFTs, structured products, endowment policies, cryptocurrencies, property etc.

Taxation

As one would expect, there are typically no, or limited tax deductions offered for the investment of these savings as well as the proceeds generated by the investments.

Unfortunately, the savings rate of South Africans is amongst the lowest in the world, with countries like India and China where the average wage is lower having significantly higher savings rates. In an attempt to encourage some savings, SARS does allow for limited tax relief such as allowing for the deduction of the first R23 800 (R34 500 for people aged 65+) on interest.

From 2015 SARS also introduced the provision that the proceeds from certain approved tax-free investments will be exempt form tax. The contributions to these types of investments are limited to R36 000 per year and R500 000 over a taxpayer’s life.

Apart from the above, the proceeds from discretionary savings are generally included in terms of the normal tax regime e.g. capital gains tax, income tax etc.

Access

Apart from any restrictions applicable to a particular investment instrument, discretionary savings are generally freely accessible.

This is obviously the main reason for people making discretionary savings choices as opposed to compulsory savings.

Investment Restrictions

Again, apart from any restrictions applicable to a particular investment instrument, discretionary savings are not subject to any restrictions, apart from the prevailing legislation.

Probably the most important issue is the restriction on foreign investments.

Protection from Creditors

Unlike compulsory savings, discretionary savings are not protected from creditors and may be attached to settle a person’s obligations.

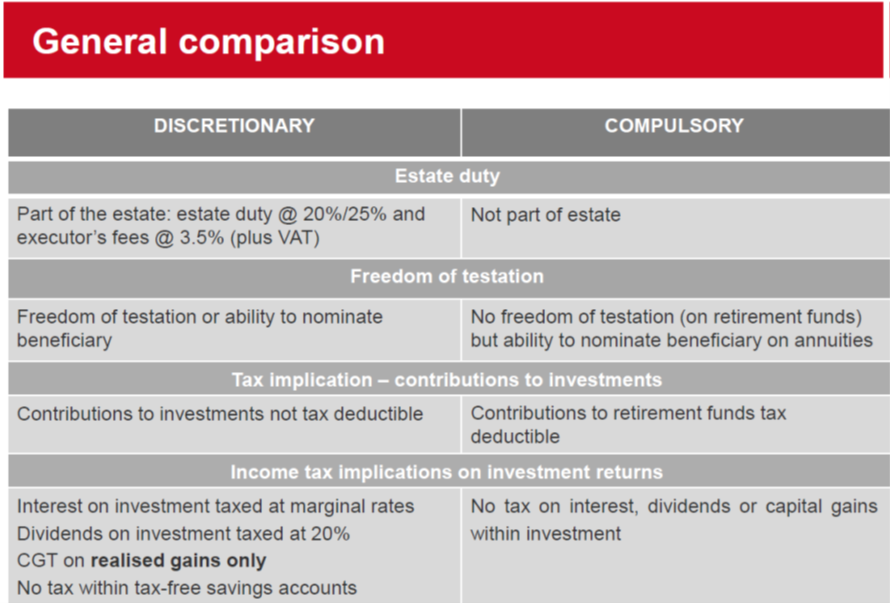

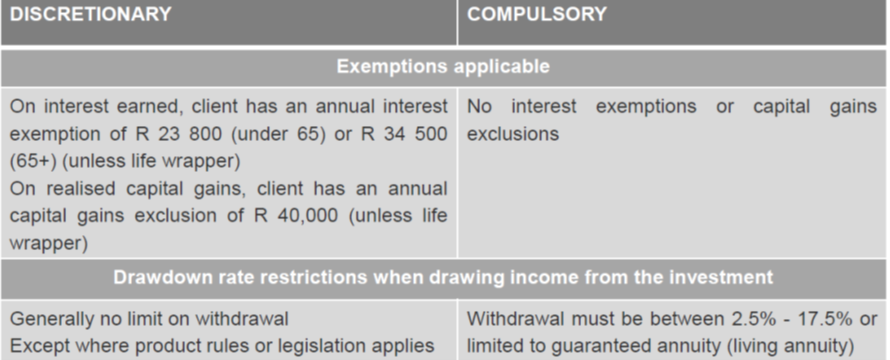

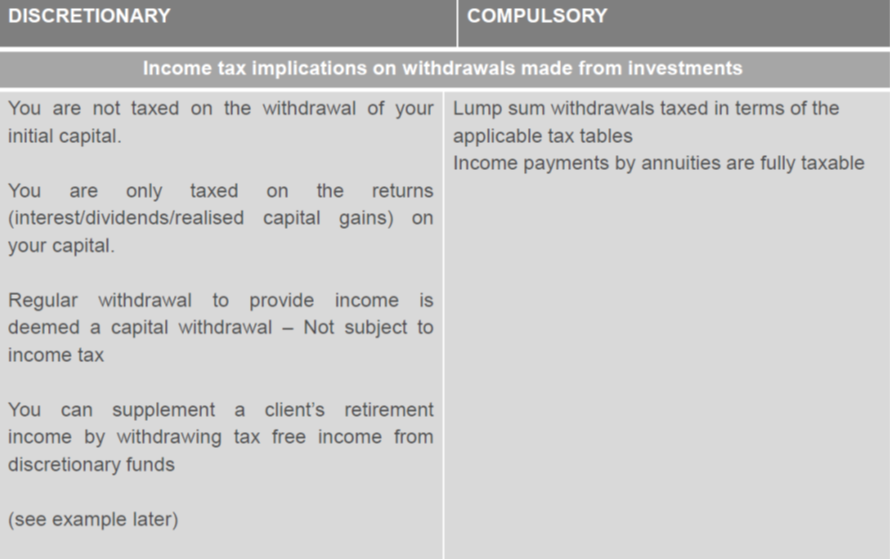

The tables below provide a comparison between discretionary and compulsory savings.

Professional Assistance

Reach out to Ubuntu Capital and a professional financial planner will get hold of you to explain everything and discuss any of your requirements.

If you would like to get a free assessment of your current retirement savings, please complete our online capture form by clicking here