Much is made in the press of the fact that only 6% of South Africans will be able to retire financially when they would like to. The alternatives include having to rely on family or others for support, having to postpone your retirement or probably the worst-case scenario of having to make do on the state pension – currently R1 880 per month.

So, what do you actually need to avoid these alternatives. Well as any economist will tell you – it depends!

While everyone’s personal circumstances are different you will need to consider several factors which will include:

- At what age are you obliged to retire, or you would like to retire.

- What you believe your life expectancy will be.

- What will be the position at your anticipated retirement regarding your financial obligations (debt!)

- What will be your monthly expenses once you retire and

- What are your retirement aspirations

Calculating the amount needed

Traditionally financial advisors have advocated that you need to have saved and amount at your retirement which is equivalent to approximately 75% – 80% of your final monthly salary multiplied by 12 years.

Another common rule used is that by utilising an annual amount in retirement that is equivalent to 4% of your retirement savings will enable your retirement savings to last for 30 years. So, using this method, 75% – 80% of your final annual salary should represent 4% of your retirement savings.

But are these “rules of thumb” still relevant? It is useful having a benchmark, but you should also consider a few factors which could undermine the application of these such as:

Retirement Age

While historically retirement ages have been between 55 to 65, life expectancy across the globe has increased by about 45% in the past 70 years. So, while it is likely that people may have a longer retirement, it is also likely people will extend their working careers in the future.

The increase in life expectancy not only creates a challenge with having to make retirement savings last longer but the increase in the forecast period your retirement plan needs to accommodate also provides more scope for error. While this impact was largely the concern of pension funds in the days of defined benefits funds, with the move to defined contribution funds the individual has now had to assume this risk.

Varying factors

Your retirement plan is based on several assumptions; however, while you can have an element of control over certain of these there are other factors which are unfortunately completely out of your hands.

You can set your preferred retirement date; estimate a retirement period and the monthly amount you believe will be adequate, which are important assumptions in trying to determine the retirement savings. But when trying to calculate what this future amount will be and what you are required to save today to achieve that amount, things like investment returns, inflation and taxation all have a major influence which you cannot control.

So, what you do?

Start

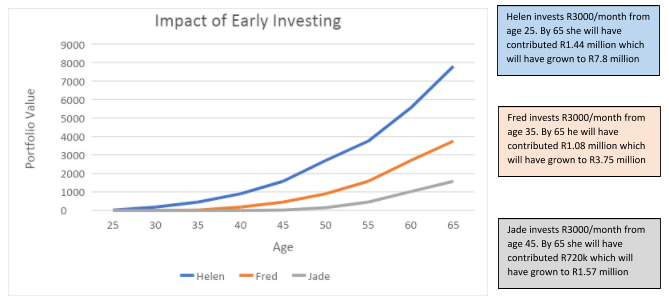

Even if you are not sure about when you want to retire etc. the fundamental lesson is that if you have not yet considered your retirement plan is to START saving as soon as is possible. The earlier you start, the less you will need to save but the significance of this impact is shown below:

- Helen invests R3000/month from age 25. By 65 she will have contributed R1.44 million which will have grown to R7.8 million.

- Fred invests R3000/month from age 35. By 65 he will have contributed R1.08 million which will have grown to R3.75 million.

- Jade invests R3000/month from age 45. By 65 she will have contributed R720k which will have grown to R1.57 million.

Not saving is readily justified by reasons such as “I cannot afford to right now”, “I will start once the children are educated”, “the market is too uncertain at the moment” etc. but the implications of this delay are massive. As Warren Buffet is often quoted as saying “Spend what you have left after saving, not save what you have left after spending”.

Make a Plan

Irrespective of your age or circumstance, you need to apply your mind to commit to some retirement planning assumptions already mentioned above e.g.

- At what age do you intend to retire?

- Estimate your retirement period.

How much do you believe you will need each month?

This will start focusing you on what you will require and what arrangements you need to start making.

Review often.

Your personal situation is constantly changing and so are the factors that you cannot control so it is critical that you review your retirement plan frequently.

The earlier you are able to identify potential issues the easier they will probably be able to be addressed.

Get assistance.

Your retirement plan is a critical part of your financial planning. Get a financial advisor on board to advise and assist you with this process. They will not only be able to give you an independent opinion, but they have probably been involved with this process a number of times.

If you are prepared to capture some information by clicking I will send you a personalised retirement plan overview – click here to capture information and get a retirement plan

Please feel free to contact my should you have any queries at derek.pettitt@ubuntucapital.